It was just a few years ago, twenty-five to be exact, that the first secure on-line purchase was completed. I certainly remember the year of 1994 when the discussion in many financial institutions was centered around how consumers would never embrace this kind of shopping and payment approach. It was a fad, a flash in the pan, and a short-lived anomaly.

For much of the 90’s I worked for Unisys, a global technology powerhouse with an enormous technology footprint within the financial services landscape. Unisys consistently boasted that its technology and equipment was responsible for processing close to 50% of the worlds checks, which represented multiple billions of checks processed annually. Thus the firm, and the financial services institutions it served, weren’t worried about the death of the checking account.

Twenty-five years later, e-commerce, as we now know it, is an enormous contributor to the global economy and is forecasted to reach $3.46 Trillion by the end of 2019 (little, if any of that revenue, will be paid via check). Entire industries have collapsed due to the shifts lead by the digitally-savvy, increasingly -promiscuous consumer. Brand loyalty is being bulldozed by digital transformation as consumers are faced with a myriad of choices and options to conduct business any way they choose, and they’re quite comfortable exercising their newfound power.

Consumers are increasingly demanding what they want, when they want it, and they have no patience to wait for a brand to get the immediacy of this need right. They move at speeds that leave organizations struggling to keep up and are lost on what to do, while the likes of Amazon, Etsy, even Facebook continue to empower the monumental evolution in consumer buying behavior.

With e-commerce playing such a significant role in the way consumers access and purchase the goods and services they seek, does it even matter who processes checks anymore? In fact, with the debit card tied to a checking account, does the consumer even need or want checks? Mobile payment options such as Apple Pay and Google Pay, or credit card issuers such as American Express, Visa, or Master Card may suggest checks are a thing of the past, and even obsolete.

But our research suggests something different …

Checks for many consumers in the United States are still being actively used. In fact, mobile payments tied to credit cards rely heavily on checking accounts in that credit card issuers regularly accept checks as a form of payment. So a physical check, in that sense, is anything but obsolete. Recent research completed by Fluent LLC indicated that checks are not only still being actively used, but for certain segments of the U.S. population, they are thriving and, along with cash, are the preferred method of payment. Fluent’s research highlights several factors that financial institutions would do well to consider:

- Consumers age 65 or older are 165% more likely to use checks most often, compared to those age 18-24.

- 34% of the time Convenience / Ease of Use is the main reason consumers claim to use their preferred payment method most often, which includes checks for the baby boomers now approaching or having reached age 65.

- 77% of mobile payment users also used cash as a payment method in the last 4 weeks preceding the research.

- 29% say Apple Pay is the most common electronic payment option used, followed by Venmo (22%).

- Consumers paying with Mastercard or Visa most often are 120% and 106%, respectively, more likely than primary Cash users to have a checking account.

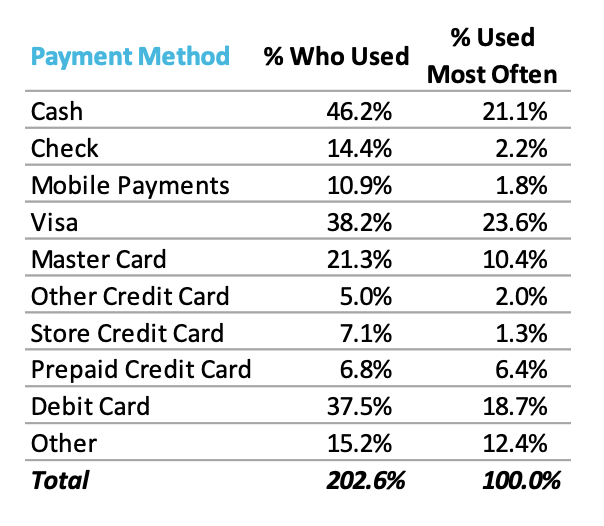

Fluent’s research points out that choice and control are in the hands of the consumer. They buy what they want, when they want it, and then pay for it in the most convenient, frictionless – and in some cases – safe way. As illustrated in this table, consumers use multiple payment options. While they may utilize preferred options frequently, there isn’t one payment method that is utilized exclusively by consumers.

What suits some doesn’t suit others.

For example, for older consumers, the drivers for staying with traditional forms of payment are primarily tied to comfort of existing benefits and security concerns. Those aged 65+ are 107% more likely to cite cash back, miles, or rewards as the reasons they use their preferred payment method most often and are 87% more likely to cite safety reasons / fraud protection. Considering this group utilizes checking 165% more of the time than that of 18-24-year-old consumers, it is safe to say check writing is alive and kicking for a significant and important portion of the U.S population.

Safety / fraud protection were also cited as one of the primary drivers for payment choice for 18-24-year olds (who were 66% more likely to have used mobile payments as their option of choice). Based on this concern simply eliminating payment options or assuming an option (such as checks) isn’t still viable may force your customers to seek alternative business relationships.

Adam Fisher, a student at Augustana College in Rock Island, Illinois and a contributor to the design and interpretation of Fluent’s research, notes “the outcome of this research, while fascinating, is also very clear – consumers pay for things the way they want, and businesses should be prepared to allow for all payment types if they want the best opportunities to compete.” Forcing a single payment type or eliminating a payment option may significantly constrict how consumers choose to patronize a business establishment, especially when it comes to certain age groups. While brands may opt to no longer accept checks, for the segment of the population that prefers this form of payment does it make sense to alienate them and force them to a competitor?

“… consumers pay for things the way they want, and businesses should be prepared to allow for all payment types if they want the best opportunities to compete.” – Adam Fisher

Choices and options are part of the way consumers expect to do business today. With $605 billion in revenue now coming from on-line transactions there is no denying the criticality of e-commerce and payment choice fueling today’s economy. Meeting the consumer where they are, and accommodating their needs in the moment they expect accommodation is critical. Expectations of accommodation extend well beyond e-commerce, as pointed out in a recent conversation with Gretchen Littlefield, CEO of Moore DM Group, a global leader in marketing solutions for non-profits, “Companies really have to align around the consumer, and develop easy, frictionless options to conduct business. Many of our non-profit customers continue to see checks as a significant payment option. I cannot see eliminating any payment option as an alternative worth pursing for the customers we serve.”

Twenty-five years ago, conventional wisdom said on-line transactions over this thing called the internet were an anomaly, a fad, and would never amount to much. That “fad” is now a global growth engine embraced by consumers world-wide. Consumers will continue to look for ways to make their lives easier. While they may not be writing as many checks, and Unisys can attest, the fact remains that consumers continue to exercise their choices when it comes to payments.

Who knows what changes we will see in the next twenty-five years and what anomalies and fads will take hold with consumers. We’re already seeing drones delivering products to our doorsteps. We’re even seeing virtual doctors and nurses making “house calls” again. And if we’re now witnessing many retailers eliminating what was one perceived to be more efficient and convenient – self-check-out stations, brands cannot assume which tried and true engagement, along with payment, options will resonate best with their consumers. What we can be sure of is the consumer will continue to define these interactions based on what suits them best.

As CEO of FLIT Consulting, Michael Fisher brings over 25 years of experience in organizational transformation through research, education, and revenue growth. He specialized in helping companies build collaborative, connected, cohesive cultures, with a commitment to personal and professional development and success. Disciplines included: progressive leadership and decision making, responsive data and analytics, nimble sales effectiveness, and agile customer data and business intelligence technology assessments.

Additionally, Michael is on the board of directors of TheCustomer.net, an online publication leading the discussion and dissemination of research and insight-led content that supports the current customer revolution, which he has coined consumerization.